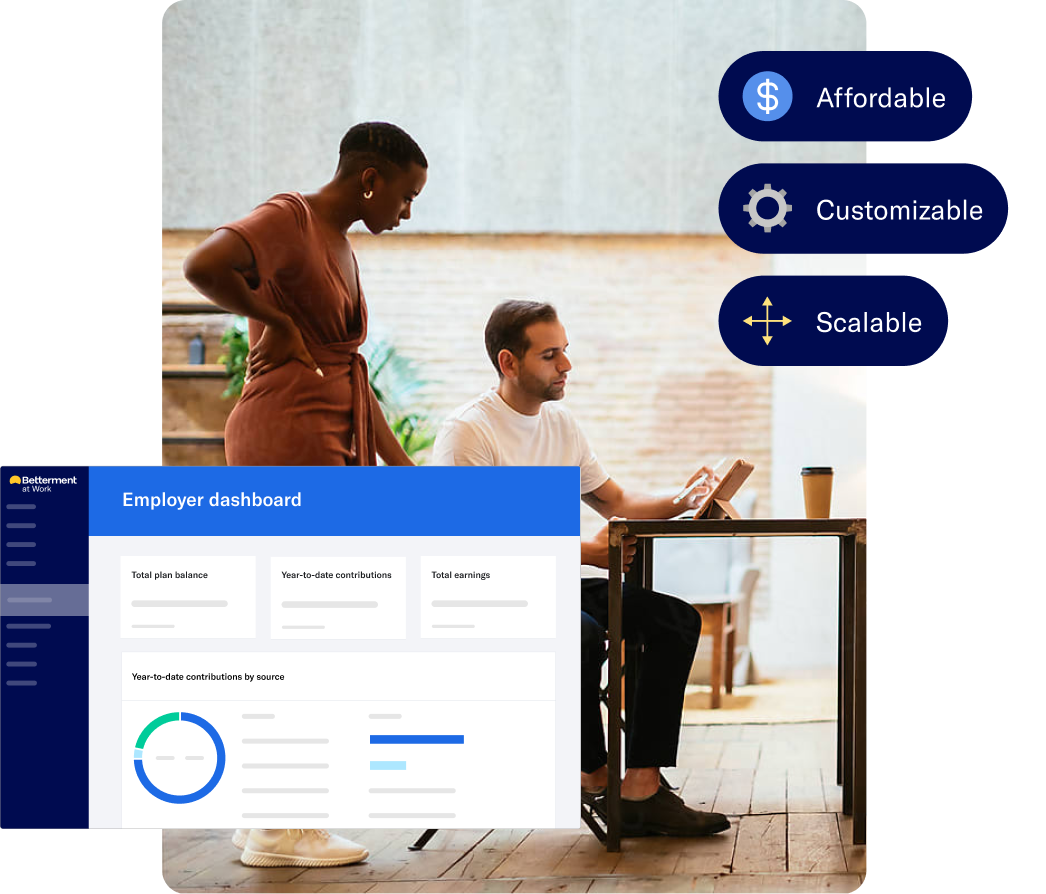

Award-winning 401(k) for small businesses

Get an affordable and customizable retirement plan designed to scale with you.

- Customizable plan features and optional employee benefits

- Service and support at every step

- Easy administration, payroll integrations, fiduciary support, and compliance testing

- All-in pricing with no hidden fees

-

Plans that match your budget.

Bypass most 401(k) compliance testing with Safe Harbor 401(k) or elect budget flexibility with a traditional discretionary match. -

Flexible plan features.

Design a plan that fits your organization's goals, from eligibility requirements, vesting schedule, profit sharing—and much more. -

Automatic enrollment and auto-escalation.

Drive plan participation by enrolling and raising employee contribution rates automatically. -

Optional 401(k) match on student loan payments.

A first-to-market offering: Increase plan participation by encouraging employees to pay down qualified student loans with a 401(k) match.

-

Dedicated onboarding specialist.

Your single point of contact to set up your new plan or convert your existing one. -

Ongoing support for your plan.

Get 401(k) administration help and answers from our Plan Support Team or a dedicated Client Success Manager whenever you need it. -

Employee support team.

Specialists are available via call, email, or chat to help resolve participant-specific needs. -

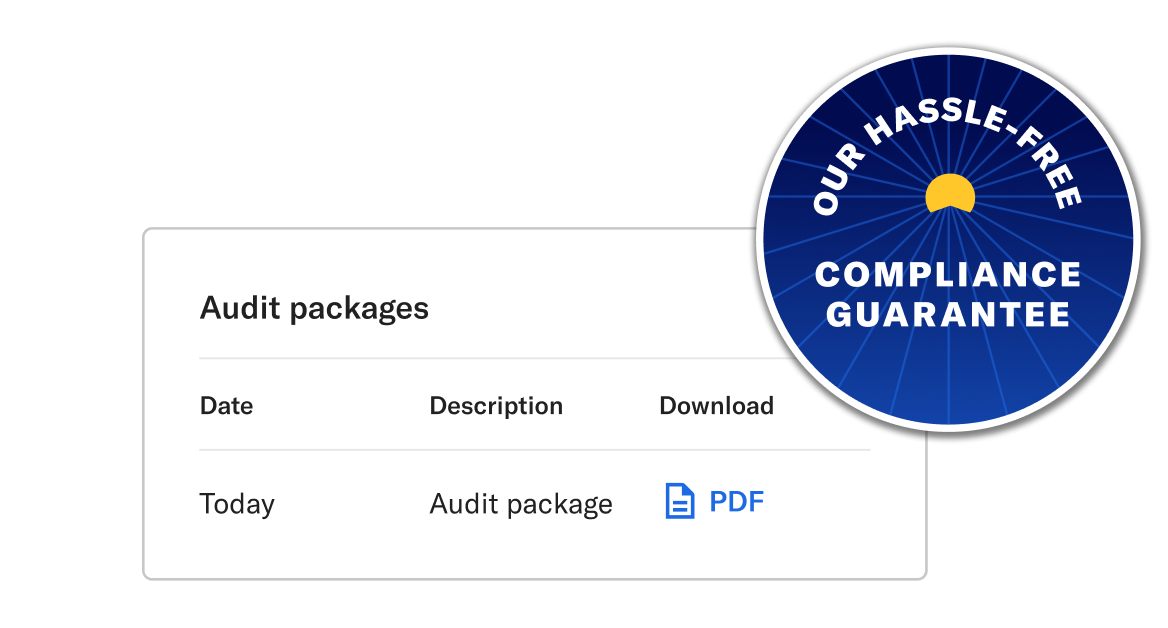

Leave your 401(k) compliance to the experts.

Our team handles annual testing, calculates contributions, and prepares signature-ready Form 5500 to help your plan stay compliant.

Our Hassle-Free Compliance Guarantee.

We guarantee that your prepared prior-year audit package will be delivered by May 31. If you are still waiting to receive it in time to file your Form 5500, we'll refund you up to $1,000 off your annual base fee.

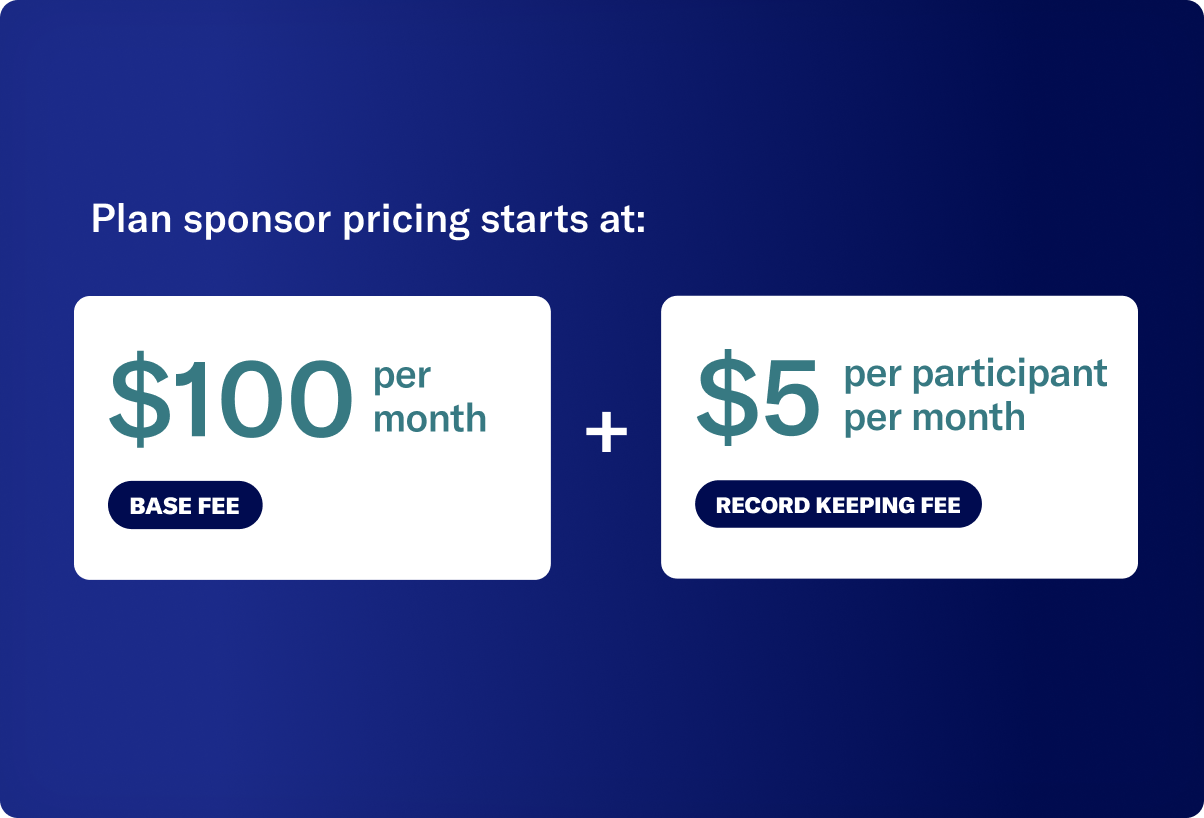

All-in pricing with no hidden fees.

Our plan features let you effectively manage eligibility and coverage, offering you more cost control. We're transparent about our fees and don't hide future costs like some providers.

With SECURE 2.0, many businesses can now take advantage of various tax credits. For new plans, this legislation can cover most of your costs for the first year.

With SECURE 2.0, many businesses can now take advantage of various tax credits. For new plans, this legislation can cover most of your costs for the first year.

Monthly base fee billed each calendar year annually. All plans include a one-time $500 implementation fee.

-

Control plan eligibility.

Decide who can participate or be excluded from your plan, like seasonal or part-time workers. -

Automatic force outs.

Automatically remove terminated employees with low balances from your plan. -

Fee flexibility.

Decide what employees pay for and what your business covers. Transfer certain plan expenses back to former employees. -

Only pay for active participants.

Reduce fees by only paying for participants who fund their 401(k)s. Participants will pay a typical management fee of 0.25%

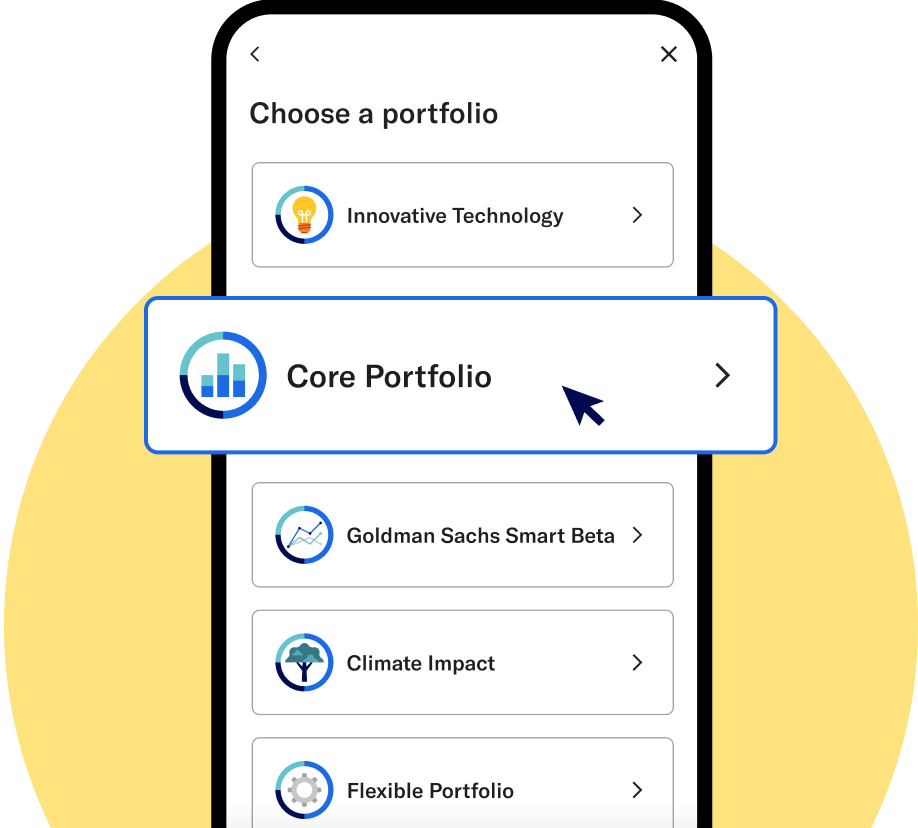

Put 14+ years of investment expertise behind your 401(k).

Our curated, expert-built portfolios make investing easy for employees. They can choose the portfolio that interests them, from sustainability to innovative technology.

If they’re an experienced investor looking for more control, a Flexible portfolio lets them adjust individual asset class weights based on their preferences.

If they’re an experienced investor looking for more control, a Flexible portfolio lets them adjust individual asset class weights based on their preferences.

Meet your future proof 401(k).